A Guide to the Different Types of Financial Advisors

1. Introduction

Financial planning is essential to the creation of wealth, wise investing, and building financial security. Whether you are a young professional savings for a home or a retired couple seeking asset planning, hiring a financial advisor is one of the most important steps in your financial journey. The hard part is not deciding whether you need an advisor. The hard part is deciding what type of advisor you need and how much it should cost.

I’m going to use those two criteria to break down the types of financial advisors and what they offer in hopes of providing you with a “road-map” to use in your own search. There are also hundreds of tools designed to connect you to the best financial advisor based on your criteria (I’ll link some below).

Other topics of interest:

Finding a Financial Advisor in Orange County [LINK]

How to Select a Financial Advisor for your Retirement Needs (eBook)

6 Days to Better Investing (The Definitive Guide to Optimizing your Investment Portfolio)

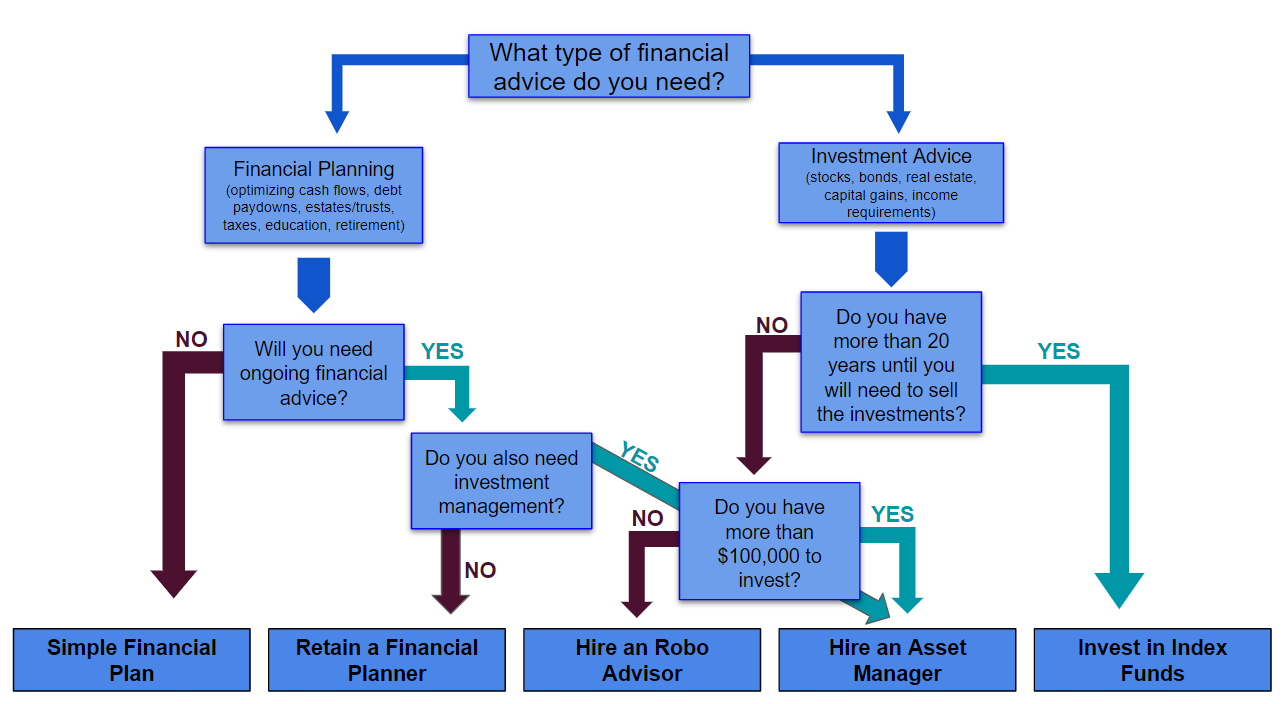

Step 1: What type of advisor is right for you?

Financial Planner

Financial planners provide a one-time financial plan and can then be “retained” to provide additional advice at pivotal financial moments (much like a lawyer is kept on retainer just in case). When you hire a financial planner, the first step in an introductory interview. They will interview you about your current financial situation, ask questions about your goals, and collect account balances and tax information. With this information, the planner will then produce a written, professional financial plan. A financial plan generally covers these topics:

- Spending, Budgeting, Monthly Saving

- Account Management (establishing trusts, retirement accounts, education accounts)

- Investing (what to invest in and how much to invest)

Once you have received your plan, it is up to you to put it into action. This means you no longer need your financial planner, but if you need ongoing advice or would like plans developed every year, you can choose to retain your financial planner.

If you choose to retain your planner, they will update your plan consistently, evaluate your investments, and advise you on decisions like buying a new house, taking out loans, or increasing your travel budget. They become a counselor, offering financial insights the same way a lawyer would provide legal advice.

Financial planners are best suited for someone who is still growing their assets by saving money rather than earning investment income. Planners also rarely have an asset minimum, which means they accept clients regardless of portfolio size. In very general terms, you should hire a financial planner if you are younger than 50, have an investment portfolio of less than $200k, and/or have the time and discipline to act on the plan outlined by your advisor.

Asset Manager

An asset manager can also be called a “holistic financial planner”, because he/she provides all of the services a planner does while also managing your investments on a discretionary basis. Because asset managers work with clients who already have established investment portfolios, financial planning becomes a secondary consideration behind asset growth and income. A manager will assume control of your assets and invest them according to a specific investment philosophy, which you will understand before you choose to invest with them. Once the relationship is established, you will have ongoing access to your advisor much like a retained financial planner, but you will not be responsible for executing the financial plan.

Because asset managers provide a more specialized, work-intensive service, they tend to be more expensive and pickier about which clients they choose to take on. Most managers have an asset minimum, which means they will not accept clients with assets below a certain threshold (anywhere between $100k and $1 million).

Asset managers are best suited for people who already have a large asset base and are seeking more specialized investment strategies. It is recommended to hire an asset manager if you need risk management (decreasing the chance of losing money), require high investment income, or lack the time/expertise to manage your portfolio on your own.

Robo Advisor

Robo advisors are automated algorithms that recommend a particular investment portfolio based on your age, goals, and risk tolerance. This is perhaps the easiest, cheapest way to gain exposure to the markets, and we recommend it to anyone interested in investing who lacks the capital to work with an asset manager. You will not receive any financial planning counsel, but it is possible to combine a robo advisor with a simple financial plan to create the lowest cost financial ecosystem. These robos are also exploding in popularity, so they are competitively priced and highly accessible. Almost every major broker dealer has a robo service, including Charles Schwab, Betterment, and Fidelity.

Step 2: How much will it cost?

The price of a financial advisor is often the determining factor for whether you hire them or not, and the range of prices in this industry is ridiculous. On the upper end, all-star hedge funds are charging more than 3% ($3k a year on $100k investment), while on the low end you can get a financial plan for only $750. There is no surefire way to determine how much you should spend, but the rule of thumb is: pay for what you need.

This diagram is very simplified and there are other elements that can be considered, but overall these are the main segments of the financial advising industry.

Simple Financial Plan

Depending on the complexity of your situation, you should expect to pay $1,000 to $2,000 once.

Retain a Financial Planner

For ongoing advice that does not include investment management, expect to pay $200 to $400 a month.

Hire a Robo Advisor

Robo’s charge 0.25% to 0.80% of assets under management, which equates to $250-$800 annually for a $100,000 portfolio.

Hire an Asset Manager

Asset managers, by and large, are charging 1.0% to 1.5% of assets under management ($1,000 to $1,500 annually for a $100,000 portfolio)

Invest in Index Funds

By far the cheapest (and riskiest) way to invest in the stock market, index funds can be held for as little as 0.07% annually. That is only $70 a year for $100,000 invested.

CONCLUSION:

Now it’s time to say goodbye and wrap up your post. Remind your readers of your key takeaway, reiterate what your readers need to do to get the desired result, and ask a question about how they see the topic to encourage comments and conversation. Don’t forget to add a Call-to-Action to turn your blog post into a marketing machine!

Congratulations! What a lovely how-to post you’ve created.